Is insurance cheaper on a new car? Well, it’s a question that pops up a lot, and the answer isn’t always straightforward. It depends on lots of things, like the type of car, your driving record, and even where you live. Let’s dive into the details and find out if that shiny new ride will save you some rupiah on your insurance premiums.

This comprehensive guide explores the factors that influence insurance costs for new cars, comparing them to used cars. We’ll also uncover potential discounts, coverage options, and how to compare insurance providers to get the best deal. So, buckle up and let’s get into the nitty-gritty of new car insurance!

Factors Affecting Insurance Costs

Car insurance premiums aren’t a one-size-fits-all figure. Numerous factors play a significant role in determining the price you pay. Understanding these elements can help you make informed decisions to potentially lower your costs. From the type of vehicle you drive to your driving record, location, and personal details, each aspect contributes to the final insurance quote.Insurance companies assess risk to calculate premiums.

A higher perceived risk results in a higher premium. This risk assessment considers a wide range of variables, including factors related to the vehicle itself, the driver, and the location where the vehicle is primarily used. The ultimate goal is to balance the costs of claims with the revenue generated from premiums.

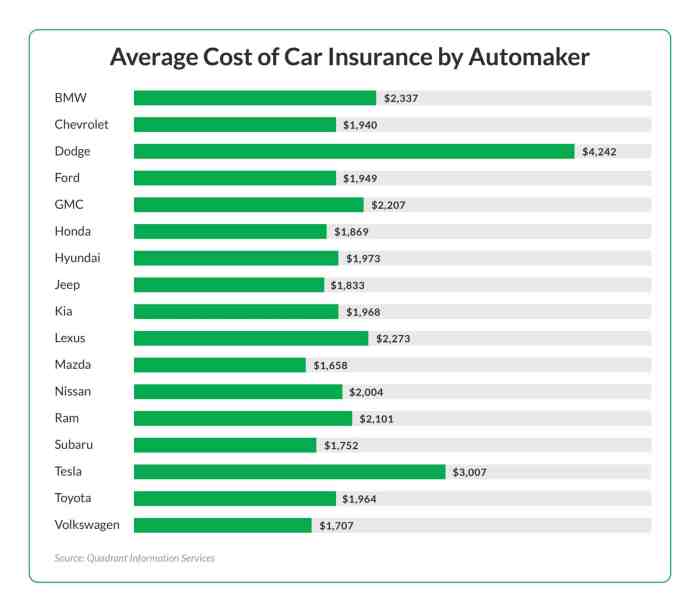

Car Model Impact on Insurance Costs

Different car models exhibit varying levels of safety and repair costs. Insurance companies consider these factors when determining premiums. High-performance sports cars, for example, often have higher insurance costs due to their greater potential for damage and repair expenses. Sedans and SUVs generally fall within a more moderate range, while economical compact cars may have lower premiums, reflecting their lower repair and replacement values.

Insurance companies also consider the make and model’s history of reported accidents or recalls, influencing the risk assessment.

Driving History’s Effect on Rates

Driving history is a crucial factor in determining insurance premiums. A clean driving record, free from accidents and traffic violations, generally leads to lower premiums. Conversely, accidents, speeding tickets, and other violations increase the perceived risk, resulting in higher insurance costs. Insurance companies analyze past driving records to estimate the likelihood of future claims.

Location’s Influence on Insurance Costs

Geographic location significantly affects insurance rates. Urban areas often have higher insurance costs compared to rural areas. This difference stems from factors like higher accident rates, increased traffic congestion, and potentially more challenging driving conditions in cities. Rural areas, with lower accident rates and fewer traffic incidents, typically result in lower insurance premiums.

Age and Gender’s Role in Insurance Rates

Statistical data demonstrates that younger drivers often have higher premiums compared to older drivers. This reflects a higher risk assessment due to inexperience and potentially higher accident rates among younger drivers. Similarly, gender-based premiums, while often controversial, can sometimes exist, based on historical data regarding driving behaviors.

Comparison of Insurance Costs Across Car Types

| Car Type | Typical Insurance Cost Impact | Example |

|---|---|---|

| Sports Cars | Generally higher due to higher repair costs, potential for higher-speed accidents, and perceived risk. | A Lamborghini might cost significantly more to insure than a Honda Civic. |

| Sedans | Moderate insurance costs, falling between sports cars and SUVs in most cases. | A Toyota Camry might have a moderate insurance premium. |

| SUVs | Moderately higher than sedans due to increased size and weight, but lower than sports cars. | A Ford Explorer might have a slightly higher premium than a Honda Accord. |

| Compact Cars | Generally lower insurance costs due to lower repair costs and perceived risk. | A Toyota Yaris might have a lower premium compared to a large SUV. |

Insurance companies use complex algorithms to calculate premiums, taking into account various factors like the vehicle’s value, driver history, location, and age. It is essential to understand these factors to make informed decisions about insurance choices.

New Car Insurance vs. Used Car Insurance

New car insurance often carries a different price tag compared to insuring a used vehicle. This disparity stems from several key factors, including the vehicle’s value, its age, and the level of risk associated with its ownership. Understanding these differences is crucial for anyone looking to secure the most competitive rates for their vehicle.

Insurance Cost Differences

Insurance companies meticulously assess risk when determining premiums. A new car, typically representing a higher initial investment, presents a higher potential for financial loss in the event of an accident or theft. This increased risk translates to higher premiums for the owner of a new car compared to a comparable used vehicle. Moreover, a new car often comes with more advanced safety features, but the absence of these features in a used car might be a consideration in the cost of insurance.

Impact of Vehicle Value

The vehicle’s value directly influences the insurance premium. Insurance policies are often calculated based on the vehicle’s replacement cost. A newer, more expensive vehicle will command a higher premium compared to an older, less valuable model. The potential financial loss in the event of a total loss is a critical determinant in insurance pricing.

Illustrative Examples

Consider two similar models, a 2024 Sedan and a 2021 Sedan. Assuming comparable driving records and coverage levels, the 2024 model will likely have a higher insurance premium. This is because the 2024 model’s replacement value is higher. A hypothetical scenario involves a 2024 model valued at $30,000, and a 2021 model valued at $20,000. The insurance premium for the 2024 model might be approximately 15-20% higher than the 2021 model, all other factors being equal.

Comparison Table, Is insurance cheaper on a new car

| Feature | New Car | Used Car |

|---|---|---|

| Vehicle Value | Higher | Lower |

| Insurance Premium | Typically Higher | Typically Lower |

| Risk Assessment | Higher potential loss | Lower potential loss |

| Safety Features | Potentially more advanced | Potentially less advanced |

| Age of Vehicle | New | Used |

Discounts and Benefits for New Car Owners: Is Insurance Cheaper On A New Car

New car owners often enjoy attractive insurance discounts and benefits. These incentives can significantly reduce insurance premiums, making car ownership more affordable. Understanding these perks can help new car owners save money on their insurance policies.

Potential Discounts for New Car Owners

Insurance companies frequently offer discounts to new car owners, reflecting the lower risk profile associated with newer vehicles. These discounts are designed to incentivize responsible ownership and reward the investment in a new, well-maintained vehicle. The potential for savings can be substantial, particularly when coupled with other discounts.

Procedures for Claiming New Car Discounts

Claiming discounts often involves providing the insurance company with specific documentation, like the vehicle’s registration or purchase agreement. New car owners must ensure they maintain all relevant paperwork, as this is crucial for verifying eligibility for discounts. Failure to provide necessary documents can lead to the denial of discounts. Insurance companies typically have clear guidelines on the required documentation, which should be readily available on their websites or through customer service channels.

Insurance Company Risk Assessment of New Cars

Insurance companies meticulously assess risk factors associated with new cars. Factors like the vehicle’s make, model, safety features, and the driver’s history are all considered. The newer the car, the lower the perceived risk of accidents and damage. Furthermore, advanced safety features in new cars contribute to a lower risk profile, which directly translates to potentially lower premiums.

These factors are meticulously evaluated in the actuarial models employed by insurance companies to determine premium rates.

Examples of Specific Discounts for New Car Owners

New car owners might qualify for discounts on insurance premiums. Examples include discounts for new drivers who are under a certain age or have completed driver’s education courses. Likewise, specific vehicle models or features may trigger discounts. For example, a vehicle with advanced safety technology might qualify for a specific discount.

Potential Savings for New Car Owners

New car owners can potentially save significant amounts on insurance compared to used car owners. The lower risk associated with new cars often translates to lower premiums. This savings potential can be substantial, depending on the specific car, the driver’s profile, and the insurance company’s policies. For instance, a new driver with a new car and good driving history might experience significant savings compared to a driver with a used car and a less favorable driving record.

Table of Discounts and Benefits

| Discount Type | Description |

|---|---|

| New Car Discount | Reduced premiums for new vehicles based on their lower risk profile. |

| New Driver Discount | Discounts for drivers under a specific age or who have completed driver’s education programs. |

| Safety Feature Discount | Discounts for vehicles equipped with advanced safety features, like airbags or anti-lock brakes. |

| Good Driver Discount | Discounts for drivers with a clean driving record. |

| Bundled Insurance Discount | Discounts for combining multiple insurance policies (e.g., home and auto). |

Insurance Coverage Options for New Cars

Navigating the world of car insurance can be daunting, especially when dealing with a brand-new vehicle. Understanding the specific coverage options available for new cars, contrasting them with those for used cars, and the associated costs is crucial for making informed decisions. This section details the standard coverage options, highlights key differences, and analyzes the impact of add-on coverages on premiums.

Standard Coverage Options for New Cars

New car insurance typically includes a combination of standard coverages designed to protect against various potential risks. These often include liability coverage, which protects you from financial responsibility if you cause damage to another person’s property or injury to them. Collision coverage protects you if your car is damaged in an accident, regardless of who is at fault. Comprehensive coverage, on the other hand, covers damages from events other than collisions, such as vandalism, theft, or weather-related incidents.

Understanding these fundamental components is the first step to ensuring comprehensive protection.

Differences in Coverage Options Between New and Used Cars

While the fundamental coverages (liability, collision, and comprehensive) are generally similar for both new and used cars, the specifics can vary. Insurance companies may adjust coverage amounts based on the car’s value and market condition. New cars, being more valuable and potentially more prone to damage due to the newer parts, often come with higher coverage limits for collision and comprehensive damage.

Used cars, with their lower value and potentially higher wear and tear, typically have lower coverage limits for these types of damage.

Types of Insurance Coverage for Different Types of Damages

Different types of insurance coverage address different types of damages. Liability insurance protects you from financial responsibility for damages you cause to others. Collision coverage pays for damage to your car in an accident, regardless of fault. Comprehensive coverage pays for damage to your car from events other than collisions, such as vandalism, theft, fire, or hail damage. Understanding these distinct coverages is essential for tailored protection.

Comparison of Coverage Offered for New vs. Used Cars

A new car of a particular model and value will typically have higher limits for collision and comprehensive coverage compared to a used car of similar value. This is because the replacement cost of a new car is higher. Insurance companies factor in this higher value and potential for greater loss when determining coverage limits for new cars.

However, this difference in coverage often reflects the higher cost of insurance for a new car. For instance, a used car with a similar market value to a new car may only have coverage up to a certain amount for collision and comprehensive, while a new car will have a higher coverage limit.

Impact of Add-on Coverage Options on Insurance Premiums

Add-on coverage options, such as uninsured/underinsured motorist coverage, roadside assistance, and rental car reimbursement, can significantly impact insurance premiums. Adding these features to your policy usually increases the cost. The premium increase varies depending on the specific coverage and the provider. For example, adding uninsured/underinsured motorist coverage to protect against drivers without insurance can increase the premium, but it’s crucial for protecting your financial interests in the event of an accident with a negligent driver.

Insurance Coverage Options for New Cars: A Cost Comparison

| Coverage Type | Description | Typical Cost for New Car (Example) |

|---|---|---|

| Liability | Protects against financial responsibility for damages to others. | $100-$300 per year |

| Collision | Covers damage to your car in an accident, regardless of fault. | $200-$500 per year |

| Comprehensive | Covers damage to your car from events other than collisions (e.g., vandalism, theft, weather). | $150-$400 per year |

| Uninsured/Underinsured Motorist | Protects against drivers without insurance or those with insufficient coverage. | $50-$200 per year |

| Roadside Assistance | Provides assistance in case of vehicle breakdown. | $50-$100 per year |

Note: Costs are examples and may vary significantly based on factors like the car model, location, and driving history.

Comparing Insurance Providers for New Cars

Securing the right insurance policy for your newly acquired vehicle is crucial. Understanding the nuances of different providers and their pricing structures is key to getting the best possible deal. This involves more than just comparing premiums; it’s about analyzing the coverage, deductibles, and potential discounts offered by each company.Comparing insurance quotes from multiple providers is essential for securing the most competitive rates.

This process often involves providing specific details about the vehicle, such as its make, model, year, and options. It’s important to remember that insurance companies assess risk differently, and understanding their criteria can help you make an informed decision.

Obtaining Quotes from Different Insurance Companies

Gathering quotes from various providers is a straightforward process. Start by identifying reputable insurance companies in your area. Next, visit their websites or contact their customer service representatives to request quotes. Crucially, provide accurate information about the new car’s specifications, as well as your driving history and location. The more accurate the data, the more precise the quote will be.

Insurance companies may use online quote calculators or require you to complete an application form.

Insurance Company Risk Assessment for New Cars

Insurance companies employ various methods to assess risk for new cars. Factors considered include the vehicle’s make, model, and safety features. A vehicle with advanced safety features might attract a lower premium, demonstrating a lower risk profile. The car’s performance characteristics, such as horsepower and acceleration, can also play a role. Driving history, particularly accident records, and location are significant factors.

Companies might also use data analytics and algorithms to predict future claims based on historical trends.

Factors to Consider When Choosing an Insurance Provider

Several key factors should guide your decision when selecting an insurance provider. Firstly, evaluate the different types of coverage offered and ensure they align with your needs and budget. Secondly, understand the deductibles and their impact on your out-of-pocket expenses. Thirdly, pay close attention to the potential discounts available. Finally, consider the company’s reputation and customer service record.

Read reviews and compare the terms of service.

Methods for Comparing Insurance Policies

Compare policies using a structured approach. Create a spreadsheet or use a comparison tool to list different insurance providers and their corresponding premiums. Include details like coverage types, deductibles, and any available discounts. By systematically listing these aspects, you can easily compare different policies and identify the best fit. Pay attention to the fine print of each policy, ensuring you understand the terms and conditions before making a decision.

Insurance Provider Comparison Table for New Cars

| Insurance Provider | Premium (Example) | Coverage Options | Discounts Offered | Deductible |

|---|---|---|---|---|

| Company A | $1500 per year | Comprehensive, Collision, Liability | Multi-car discount, Good student discount | $500 |

| Company B | $1700 per year | Comprehensive, Collision, Liability, Uninsured Motorist | Multi-car discount, Defensive Driving Course | $1000 |

| Company C | $1350 per year | Comprehensive, Collision, Liability | Bundled insurance discount, New Car discount | $500 |

Note: Premiums are examples and may vary based on individual circumstances.

Tips and Strategies for Reducing New Car Insurance Costs

Owning a new car is an exciting experience, but the associated insurance costs can sometimes be a significant financial burden. Understanding strategies to lower premiums is crucial for managing these expenses effectively. Implementing these tips can save you money and ensure you’re well-protected without breaking the bank.A well-maintained driving record and responsible driving habits are key factors in securing favorable insurance rates.

Proactive measures like taking advantage of available discounts and comparing quotes from different providers can further optimize your insurance expenditure.

Maintaining a Superior Driving Record

A clean driving record is paramount in securing competitive insurance rates. Accidents and traffic violations directly impact insurance premiums. Consistent safe driving habits are essential for building and maintaining a positive driving history. A clean record demonstrates responsible behavior on the road and reflects a lower risk profile to insurers. This translates into potentially lower premiums.

Driver Education Programs

Driver education programs are valuable resources for new drivers and experienced ones alike. These programs offer comprehensive training in safe driving techniques, accident avoidance, and defensive driving strategies. Completing a recognized driver education program can enhance your driving skills and knowledge, potentially leading to a reduction in your insurance premiums.

Safe Driving Practices

Safe driving practices encompass a wide range of behaviors that contribute to accident prevention. These include adhering to speed limits, avoiding distracted driving, and maintaining a safe following distance. Regularly practicing safe driving techniques not only reduces the risk of accidents but also demonstrates responsible driving habits, which can favorably impact insurance premiums. Using seatbelts, avoiding alcohol and drugs while driving, and ensuring proper vehicle maintenance also contribute to a safer driving profile.

Actionable Steps to Reduce Premiums

- Maintain a Clean Driving Record: Avoid any traffic violations or accidents. This is the single most significant factor in controlling your insurance costs.

- Take a Defensive Driving Course: Many insurance companies offer discounts for completing defensive driving courses. These courses teach you techniques to avoid accidents and improve your driving skills.

- Compare Insurance Quotes: Don’t settle for the first quote you receive. Shop around and compare quotes from multiple insurance providers. This allows you to identify the most competitive rates for your situation.

- Consider Bundling Insurance: If you have multiple insurance needs (home, auto, etc.), consider bundling them with the same provider. Many companies offer discounts for bundling.

- Review and Update Your Coverage Needs: Regularly evaluate your coverage needs and adjust your policy accordingly. Ensure you have adequate coverage but avoid unnecessary extras that drive up premiums.

- Pay Premiums in Full and on Time: Consistent payments demonstrate financial responsibility, which can positively impact your insurance rates.

Last Recap

In conclusion, while a new car might seem like a no-brainer for savings, the actual cost of insurance isn’t always clear-cut. It’s a balancing act between the factors mentioned, and finding the best deal requires comparison shopping and understanding your own situation. Hopefully, this guide has given you a clearer picture of the ins and outs of new car insurance, so you can make an informed decision.

FAQ Overview

Is insurance always cheaper on a brand new car?

No, not necessarily. While a new car might have lower premiums in some cases, factors like your driving record and the car’s value play a significant role. Sometimes, a well-maintained used car can have lower premiums.

What discounts are available for new car owners?

Many insurance companies offer discounts for new car owners, often tied to specific programs or features. These could include new driver discounts, safety features discounts, or loyalty programs. Check with your insurer for specific details.

How does my driving history affect my new car insurance?

Your driving history, including any accidents or traffic violations, is a crucial factor in determining your insurance rates. A clean driving record generally translates to lower premiums.

Can I get a better insurance quote from a different provider?

Definitely! It’s always wise to compare quotes from multiple insurance providers. This helps ensure you’re getting the best possible rate for your new car.